However, in the non-credit domains, such as health insurance, investment products or retirement products, the inclusion record has been far less cheerful—indeed, it has barely even started.

There is a story to be told about why the discrepancy is so stark between credit and every other kind of financial product. And, even within credit, there is not always agreement between stakeholders as to whether financial inclusion has truly succeeded or not. This latter disagreement is the subject of this piece, which also touches upon the other inclusion story—non-credit products.

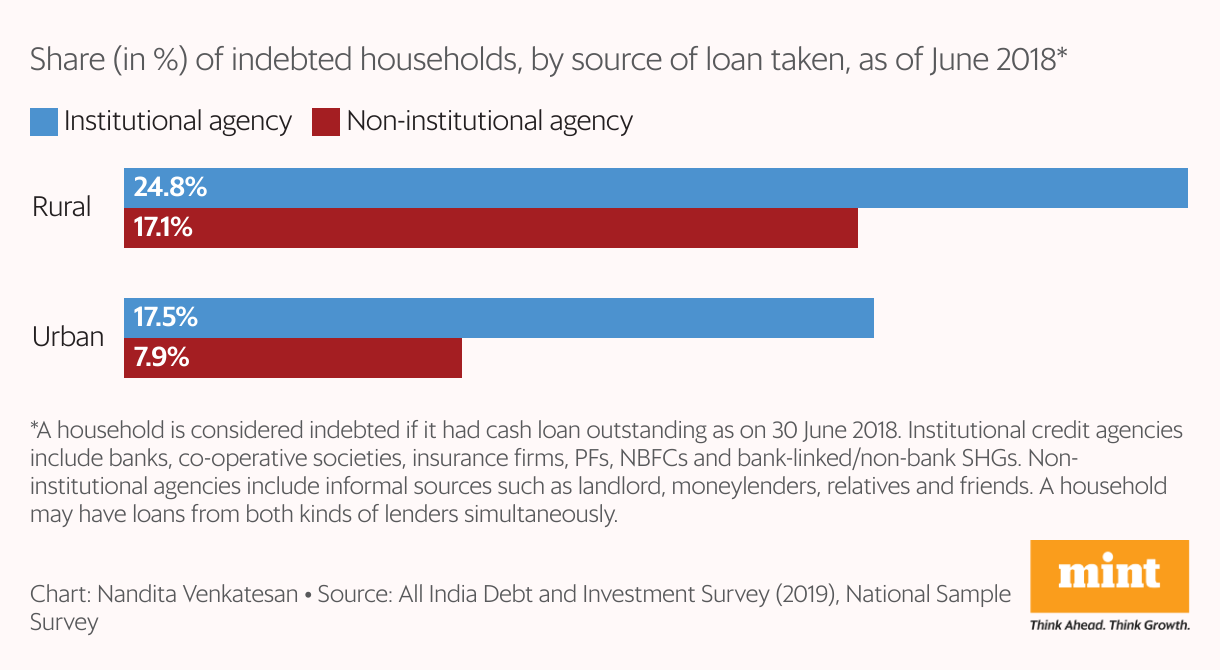

Data from the 2021 All India Debt and Investment Survey (Aidis) suggests that between 2013 and 2019, rural households in India increased their reliance on formal sources of credit by 10 percentage points. At the same time, informal sources continued, as of 2019, to constitute a full 34% of rural households’ outstanding debt. There is a variety of hypotheses that these numbers might cause us to formulate.

I will focus on two of them. The first is perhaps access to formal credit remains a significant issue for India’s rural poor. The second is perhaps formal and informal credit are not substitutes but complements. The interesting thing to note is that these two hypotheses are not necessarily competing ones, but could both be true. If that were the case, what might policymakers and regulators take away from that possibility?

The 2021 Aidis data indicate that as of 2019, 35% of rural households in India had some quantum of debt outstanding—18% had debt from formal sources only, 10% had debt from informal sources only, and 7% had debt from both sources. This implies that 25% of Indian rural households were relying on formal sources of credit in 2019. Whether or not that number is high enough, it is the case that it hides a great deal of state-wise variation. In only 10 states, more than 25% of rural households relied on formal sources of credit, and the number breaches 40% only in the three states of Andhra Pradesh, Kerala and Telangana. In 15 states, less than 15% of rural households relied on formal sources of credit.

Clearly, access to formal credit remains an issue that requires policymakers’ attention. Yet, regular numbers on the penetration of total formal credit at the district or state levels are hard, if not impossible, to come by in the public domain. Without such numbers, we cannot focus our attention more keenly towards helping formal credit become available to under-served parts of the country.

At the same time, it is important to recognize that the financial lives of the poor are radically different from those of the middle- and high-income segments of the population. Relative to the latter segments, the poor have incomes that are both unstable and insufficient. One way to appreciate this point is to look at monthly data rather than annual data. When one does this, one finds that a household may be judged as non-poor, or above the poverty line, on an annual reckoning, i.e., by taking the total annual income and comparing it to the poverty threshold defined in annual terms. But, the same household could appear as poor for more than six months of the year when the monthly income is compared to the poverty threshold now defined in monthly terms. That is, many poor households experience episodic poverty, moving in and out of poverty many times during the course of the year.

The obvious implication is that the poor suffer from cash flow deficits almost routinely, and therefore much of their borrowing is for consumption smoothing—they are not borrowing for conspicuous consumption that regulators and commentators usually worry about, but rather borrowing for consumption to sustain themselves at a minimal required level. For that reason, such borrowing also most likely enables household enterprise activities because personal and business expenses are not easily distinguishable in the case of poor households. The canonical case here is that of a poor agricultural household with highly seasonal income patterns that is consumption-smoothing within the year to remain above the poverty line.

Regulatory mandates for formal institutions require them to disburse credit on the basis of income assessments. Yet, it is cash flow that is the proper input variable here. The far-reaching effects of this discrepancy cannot be overstated. On the one side, it means that even as formal credit becomes available, the poor do not stop relying on informal sources.

On the other side, it means that credit disbursements are wrongly calibrated to the borrower’s requirements, since the condition for borrowing (cash flow deficits at a high frequency) is not aligned with the condition for lending (income sufficiency at a low frequency). As such, this kind of mismatch can quickly invite the threat of delinquency, inspiring once again a reliance on informal sources to repay formal debt. In other words, formal and informal debt become complements, not substitutes.

In conclusion, if it is true that many rural households in India still do not have access to formal credit and also true that formal credit does not and may not necessarily replace informal credit, then the policy problem is multi-layered. Last-mile access needs to be prioritized, but also new forms of credit decisioning need to be encouraged to protect the borrower from falling into a debt spiral. Therefore, last-mile access and customer protection should be simultaneous future policy priorities in the financial inclusion domain.

Indradeep Ghosh is executive director, Dvara Research. Views are personal.

Also Read: Ajay Tyagi: Capital markets set to play their role in India development journey